State of India's Carbon Markets

Why do India's carbon markets lack agricultural depth and farmer agency? What can we do about it?

Editor’s Note: This is an adapted version of a talk I gave at an UNDP webinar few moons ago. I am sharing it publicly here outside the paywall with the hope that those who are working inside India’s carbon markets react/respond to my diagnosis and share deeper context and actionable recommendations that address the challenges I talk about here.

Here is the geography I cover in my talk:

Why does India’s carbon market lack agricultural depth and farmer agency? -> What are the six systems principles that underpin India’s carbon markets - > Two sets of Warm Data worth meditating upon to address lack of agricultural depth- > Four feedback Loops that underpin farmer exclusion in carbon markets→ Can APCNF build India’s MRV standard for natural farming?

If you don’t want CC hassles, you are most welcome to use paypal or UPI (venkat.raman.kr@icici) and pay the annual subscription (8500 INR/95 USD) with your email in the comment. I will enable access immediately.

P.S. Supporting this work doesn’t have to come out of your pocket. If you read this as part of your professional development, you can use this email template to request reimbursement for your subscription

State of India’s Carbon Markets

Setting the Context

After China, India is the second-largest carbon credit producing country in the world. A Verra registry analysis shows China with 1,115 projects, 489 of them registered, and India with 1,007 projects, 519 of them registered.

But here is the thing. India has scale in the voluntary carbon market, but not agricultural depth.

Agriculture is about 0.2 percent of India’s issued credits, while renewable energy accounts for roughly 87 percent, a split the underlying Berkeley registry data confirms. A C-GEM landscape study puts India’s 132 dedicated agriculture projects at just 0.40 million tonnes of CO2 issued between them.

The agri-food subset is even thinner.

Of the 242 agri-food projects registered under Verra and Gold Standard by the end of 2024, only 21 had actually earned credits. India as a whole was about 4.1 percent of the global voluntary carbon market by revenue in 2023.

Much like us exporting low-quality rice — strike that, exporting water to be precise — to African countries, we are doing the same in carbon credits.

Here is where things get interesting.

Agriculture is the only sector in India’s voluntary market where almost every credit issued has already found a buyer with a near-zero unsold buffer. Demand is not the bottleneck. The architecture is. Today, it is almost impossible to let a farmer produce a credit in the first place.

If agriculture can sequester carbon, reduce methane, improve soil health and generate farmer income, why should farmers not participate in carbon markets with a steady demand? Before we unpack this question with all its complexity, let’s first start with basics.

What is a carbon credit?

One credit stands for one tonne of carbon dioxide or its equivalent in another greenhouse gas such as methane. That tonne can come from two very different kinds of project.

An avoidance credit rewards an emission that was prevented. The methane a rice farmer keeps out of the air by draining a flooded paddy instead of leaving it submerged. Or by changing his practice to direct-sowing method.

Now wait. Didn’t the farmer originally do this method, before they were advised to switch by the so-called “experts” during the times of green revolution, back in the sixties?

A removal credit rewards a tonne actually pulled out of the air and stored in a tree, in soil, or in biochar. Both sell as a single credit, yet a removal is harder, more durable and that gap is where things get complex. A buyer pays for that tonne to offset their own emissions.

The whole system was built decades ago for large industrial emitters like power plants and steel mills. It learned to measure a smokestack, but never a smallholding farmer’s predicament.

Six Systems Principles Underpinning India’s Carbon Markets

On paper, India has far more potential sellers of carbon than buyers. The country has roughly 146 million farm holdings, and beyond them sit forest communities and wetland stewards, a vast pool of land that could store or avoid carbon. Buyers at home are thin by comparison, because domestic corporate demand is still young and most appetite for Indian credits comes from abroad.

Systems Principle #1: There are more potential sellers (farmers, forest communities, wetland stewards) than buyers in India’s domestic carbon market.

The reasons are obvious. The market reads a factory easily than a farm. A factory has one chimney and a meter. A farm has fragmented plots, mixed crops and soil that changes across every cluster, depending on its topography

Systems Principle #2: India’s carbon markets are legible to large industrial emitters and almost completely illegible to smallholders.

Information and communication gaps are the central obstacles for smallholders starting all the way from how a credit is calculated to which market channels even exist. A C-GEM survey of 94 civil-society groups reports that 93 percent of the barriers are knowledge gaps, and that 84 percent had never joined a carbon project even though 41 percent had been approached by a developer.

Why is this the case? Ultimately, it boils down to risk bearing architecture.

Here is how carbon markets work in ag contexts. A project developer signs up farmers, runs the measurement and sells the credits. The farmer supplies the practice change that creates the credit. The developer captures the margin.

The farmer becomes the asset rather than the partner.

Europe’s regenerative farmers put a number on this. They modelled a 100-hectare project, and after a permanence buffer, a project buffer and a developer commission of around 35 percent, the farmer was left with roughly €20 per hectare a year in the optimistic case.

India’s best project tells the same story.

In January 2026, Grow Indigo’s Aadi project became India’s first high-integrity soil-carbon issuance under Verra’s rigorous VM0042 method, covering about 30,000 acres across Punjab and Haryana and generating more than 50,000 credits. This is the gold-standard with real science and satellite-backed verification. Even here, the company estimates the carbon revenue lifts farmer income by only around 7 percent. The credits fetch $40 to $60 globally, with no domestic benchmark yet.

Systems Principle #3: In the current project developer model, the farmer is the asset. The developer captures the margin.

Carbon can top up a farm’s income, but it cannot be the reason a farmer rebuilds her whole practice. Can the market see farmers as more than carbon-bearing assets?

Systems Principle #4: Carbon Markets shall always remain supplementary income for farmers

Carbon markets are in throes of change.

India is moving from an informal voluntary market to a regulated one under the Carbon Credit Trading Scheme. Nine energy-intensive industrial sectors now face binding compliance targets. Agriculture sits outside that in a voluntary offset track with government-defined rules but no mandatory demand. Soft demand keeps the price low. A low price gives the farmer no reason to change.

But there is a deeper problem that is often not spoken about.

A CO2 certificate promises permanence and soil carbon cannot deliver it.

Healthy soil is alive and microbes constantly build and break down organic matter. Any carbon you add to the soil will, in time, be eaten by those microbes and released again as carbon dioxide or methane.

The carbon does not stay put. Nature loves to recycle carbon. The systems we have built around soil carbon treat soil carbon as a stock, a quantity locked in a vault, when in nature it behaves as a flow, a river moving through the ground.

Systems Principle #5: CO2 certificates are not the right instrument for agriculture.

A certificate that pays for permanence is the wrong tool for something impermanent by design. Few who understand this are walking away.

Climate Farmers built Europe’s first internationally approved soil-carbon methodology and then stepped back from the market, judging that integrity had become too costly to deliver.

The reasons are obvious. We are trying to flatten a living system into one number.

Systems Principle #6: We are attempting to use a highly sophisticated, data-heavy financial instrument (Carbon Credits) to solve for a primitive, illiquid asset class (soil and trees).

Regeneration touches soil biology, water, biodiversity and farmer livelihoods all at once and a single CO2 score captures none of that. You cannot read a soil’s health from one figure any more than you can read a person’s health from their weight.

And there is the additionality clause.

A project earns credits only for going beyond business as usual. The farmer who switched to zero tillage last year qualifies. The farmer whose family has farmed regeneratively for three generations does not, because for her it is already baseline. The market has strong case of recency bias: It rewards the recent convert and shuts out the person who was right all along.

How do we address these challenges?

Two Sets of Warm Data Worth Meditating Upon

Warm data' is Nora Bateson's term for context-rich, relationship-embedded information that gets lost when you reduce a system to metrics. Hot data is the number — 0.2% agriculture credits, 99% of farmers received nothing.

Warm data is the why behind the number. You could argue that the carbon market runs on cold data, while regeneration needs the warm kind.

Europe’s regenerative farmers’ position paper on soil carbon markets sets out six redesigns.

Replace the single CO2 score with outcome indicators for soil, water and biodiversity.

Build tiered measurement, so the paperwork burden scales with the size of the farm.

Reform additionality to reward continuous improvement, not just new conversions.

Separate regenerative livestock from industrial livestock in the accounting.

Restructure the finance to pay farmers earlier and share the transition risk.

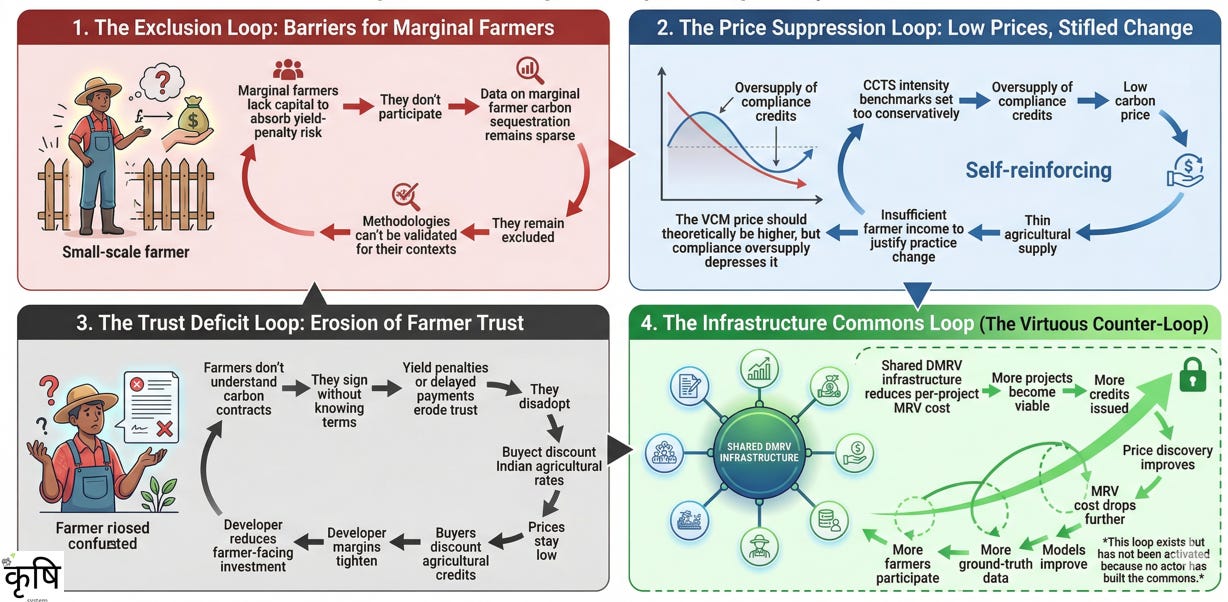

Four Feedback Loops

When you ponder about why carbon markets are stuck, you eventually end up at three feedback loops that keep the market stuck. The fourth one is the possibility that awaits when we wear the ecosystem hat.

Exclusion loop

Marginal farmers cannot absorb the risk of a yield dip, so they stay out. Because they stay out, we gather no data from their fields, and because we have no data, the methods never learn to measure them. So they stay excluded next season and the one after.

In carbon projects studied across Haryana and Madhya Pradesh, Scheduled Caste and Scheduled Tribe households held only 5 percent of the land against 17 percent in neighbouring villages, and women were about 4 percent of participants despite doing most of the farm labour.

Price-suppression loop

Conservative benchmarks under the compliance scheme flood the market with easy credits and oversupply pushes the price down. Low carbon price means insufficient income to justify farmer practice change. Thin agricultural supply means VCM prices for agricultural credits should theoretically be higher. Unfortunately, the compliance oversupply depresses even that.

Price divergence is extreme globally — from under $6/tCO₂e for low-quality avoidance credits to $1,000+ for tech-based removals.

Trust-deficit loop

Farmers sign contracts they were never equipped to read. With yield penalty or a delayed payment, trust breaks further. They drop out, buyers discount Indian agricultural credits, developer margins tighten, and investment in farmers falls further. Registry timelines of 4–5 years erode farmer confidence before any payment materialises. The C-GEM study found that interviewees cannot answer farmer questions on amount, timing, or guarantee. A farmer anecdote from Haryana paints the reality starkly.

Jitendra Singh practiced non-flooded rice cultivation for three years and had not received a single rupee. Not because the developer was dishonest. But because the system takes that long.

The Infrastructure Commons Loop

This loop is the reason I am still optimistic about carbon markets and see some ecosystem gameplay in context with the work I do at Krishi.System.

Shared DMRV infrastructure reduces per-project MRV cost. Lower cost makes more projects viable. More projects mean more credits issued. More supply improves price discovery. Better prices attract more farmers. More participants generate more ground-truth data. Better data improves models. Better models reduce MRV cost further.

Who is building a shared digital MRV commons on Agristack? Let’s take the case of regenerative agriculture in India. There is no single, purpose-built MRV standard for Regenerative Agriculture in India yet.

Take the case of natural farming which is getting adequate traction, thanks to state-led efforts such as APCNF.

We are dealing with three levels of district verifications.

The first is practice compliance. Is this farmer actually chemical-free and following the Natural Farming methods package? On the government side, the National Mission on Natural Farming uses a farmer-friendly certification managed by NCONF under the Participatory Guarantee System (PGS-India), with real-time geo-tagged monitoring through the NMNF portal.

As has been reported in several states, Regional councils are being pressured to register thousands of farmers quickly. The haste could dilute the credibility of the natural farming label. Certification runs roughly Rs 1,500 to 2,000 per hectare per year.

The second is climate outcome: soil carbon, methane, emissions.

India has borrowed, not built, its own.

The credible MRV players run on international methodologies like ISO 14064-2 and Verra's VM0042. On the soil-carbon side, Boomitra became the first developer to register an Indian project under VM0042, and rice-focused outfits like Mitti Labs and CarbonMint use satellite-plus-sensor digital MRV feeding into voluntary registries and, increasingly, India's national carbon trading portal. None of these is natural-farming-specific. They verify a carbon claim, not an NF-practice claim, and the two are not interchangeable.

The third is market/produce claim — residue-free, traceable to a plot. Private players are creating their own data silos.

We need a stack that brings these three levels of verification claims together.

Who is building India’s RegenAgri stack?

In April 2025, RegenAgri launched its Carbon Insetting Standard 2.0. It has A) practice-certification layer against regenerative criteria, B) Updated soil organic carbon quantification combining direct measurement, modelling, and hybrid methodologies C) Monetization rail where participating farms generate third-party-verified carbon insetting units. RegenAgri anchors its carbon accounting to GHG protocols and IPCC guidelines.

Can APCNF build RegenAgri equivalent for India?

APCNF has the practice model at state scale. It has the outcome evidence machinery others lack. What APCNF hasn't done is codify that into a transferable, third-party-auditable MRV protocol that a carbon buyer or a Sarkar registry could plug into. It generates evidence; it hasn't yet productized a standard.

Can APCNF do it? I hope they do:)