What should India download from Netherlands' blueprint?

State of Agritech - 16th July 2026

In Today’s Edition:

1/ What should India download from Netherlands’ blueprint?

The second largest agricultural exporter on Earth is extraordinarily good at producing, processing, trading and exporting high-value agricultural products. What should India download from Netherlands’ blueprint? And what it shouldn't?

2/ Double Clicking on PRAGATI: Can India’s Largest Privately Held Agri-Entrepreneurship Program deliver the goods?

Governments, Corporates and Global Foundations are joining hands to train 20,000 agri-entrepeneurs who will serve 200,000 smallholders. The initiative targets a 30% rise in farmer incomes and a 15-20% yield boost in paddy, maize and potato, with regenerative practices adopted by at least a fifth of participating farmers. Are these targets feasible? What would it take to deliver these targets?

If you don’t want CC hassles, you are most welcome to use paypal or UPI (venkat.raman.kr@icici) and pay the annual subscription (8500 INR/95 USD) with your email in the comment. I will enable access immediately.

P.S. Supporting this work doesn’t have to come out of your pocket. If you read this as part of your professional development, you can use this email template to request reimbursement for your subscription.

Upcoming Krishi.System Event:

1/ What should India download from Netherlands’ blueprint?

A recent paper from Nature asks an extremely important question: Is Netherlands feeding the world? Or is the world feeding Netherlands’ livestock?

Before we answer this provocative question that carries deep political ramifications, let’s set the context.

The Netherlands is extraordinarily good at producing, processing, trading and exporting high-value agricultural products. It has built one of the world’s most sophisticated agri-food ecosystems: greenhouses, seed systems, logistics, cold chains, knowledge institutions, farmer training, water control, precision horticulture. It has cracked what it takes to unleash dense collaboration between government, companies and research.

The Dutch model offers a seductive answer to every country struggling with fragmented farms, poor quality, weak logistics and climate stress: Make agriculture scientific, controlled, export-oriented and institutionally coordinated.

And India has been salivating.

Punjab’s chief minister, after touring the World Horti Center in Westland, announced plans for a horticulture learning centre built on the same lines, as Punjab’s path to redemption from its water-guzzling crops

The eighth Joint Working Group on agriculture between the two countries recorded that bilateral Centres of Excellence have demonstrated advanced technologies, produced quality planting material and trained thousands of farmers, and that both sides now want to scale the model into more states and more horticulture subsectors.

This year’s India–Netherlands joint statement went further, committing to Clean Plant Centres and an Indo-Dutch Centre of Excellence on dairy training in Bengaluru.

The Dutch government’s own India-facing agriculture page calls the offer a ‘Dutch Integrated Approach’, where companies, government and research institutes work together to squeeze more out of scarce resources.

The industry cluster HortiRoad2India expects India’s first fully operational high-tech greenhouse to begin production by the end of this year.

But the question remains. What can India exactly learn from Netherlands? And more importantly, what should India NOT LEARN from Netherlands.

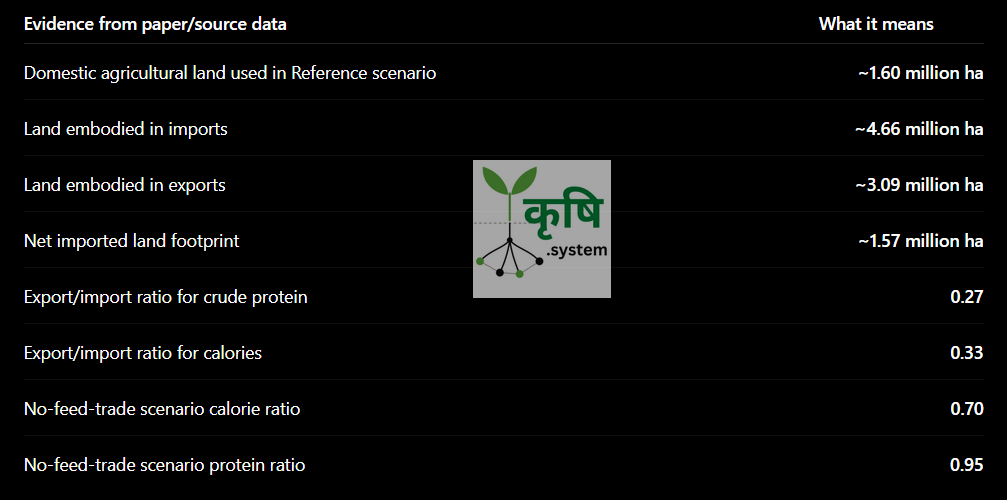

When we peel the mythology surrounding the Dutch model and go one step deeper, we discover this uncomfortable duality: The Netherlands is the second-largest exporter of agricultural goods on earth. It is also, on balance, an importer of calories and protein.

Here is the data in plain sight.

Dutch agriculture uses about 1.6 million ha inside the Netherlands, but current production, consumption and exports also depend on about 4.7 million ha abroad, largely for food and animal-feed imports.

How the paper arrived at this insight is deeply fascinating.

Ben van Selm, Imke de Boer and colleagues at Wageningen ran the Dutch food system through an agroecological model. They asked how many people the Netherlands could actually feed from its own soil. The answer is roughly its own population. But there is a catch here: Only if the crops the country cannot grow are swapped for locally available substitutes. And that comes with its price tag. That alone would consume every available hectare. Nothing would remain for exports, for bio-based materials, for bioenergy, or for nature.

Measure Dutch farming in euros and it looks like a miracle. Measure it in land, feed, calories and protein and the miracle thins out. This distinction acquires deep political implications when you contrast India’s context with Netherlands’.

The Netherlands is a dense trading economy with high capital, high institutional trust and a deeply integrated European market.

India is a vast, unequal, smallholder-heavy food system where agriculture is simultaneously livelihood, food security, ecological management and political economy.

India is importing the Dutch model at the precise moment Dutch scientists are dismantling the narrative that sells it. As de Boer puts it, the Dutch role no longer lies in high-volume exports, and the country's real strength may lie in planting material, knowledge and innovations that help other countries produce and consume food more sustainably.

Net net, the moral of the story is this.

Protected cultivation may be useful for perishables, quality, urban supply chains and farmer income, but it should not be sold as a national food-security substitute.

India should copy the learning architecture: research–industry–extension–farmer feedback loops. It should not copy the resource footprint blindly.

Every Dutch-inspired intervention in India should ship with a public balance sheet, published annually.

Land used and displaced. Water drawn and saved. Energy intensity. Nutrient and plastic flows. Import dependence. Farmer income and farmer debt. Calories and protein actually added to the Indian food system.

Punjab has been trying darnedest to escape its groundwater trap. It cannot afford to not have the indicator that shows where the water went. India should import Dutch discipline. It should leave the blind spot in Westland.

2/ Double Clicking on PRAGATI: Can India’s Largest Privately Held Agri-Entrepreneurship Program deliver the goods?

What is the purpose of agri-entrepreneurship in smallholding contexts?

Can agripreneurship simultaneously transform the incomes of smallholders while building viable livelihoods for the entrepreneurs ? And can this model be built at scale, bringing together Governments, Foundations and Corporations, to deliver the regenerative outcomes?

These are some of the gnarly questions that I encounter when I study PRAGATI, as their press release suggests, “India's largest privately led agri-entrepreneurship programme”

What are we essentially dealing with?

Twenty thousand agri-entrepreneurs. Twenty lakh smallholders. Twenty thousand village kiosks. Eight states which already have agripreneur networks running: Madhya Pradesh, Bihar, Uttar Pradesh, Assam, West Bengal, Jharkhand, Maharashtra and Rajasthan.

And the targets look ambitious at first blush, until you examine AEGF’s body of public work.

A 30% rise in farmer incomes

A 15 to 20% yield boost in paddy, maize and potato

Regenerative practices adopted by at least a fifth of participating farmers

Financial inclusion for half.

For an ambitious program of this kind, no rupee figure was announced. No scheme document. No published MoU. The version carried by Business Standard runs under an advertorial disclaimer.

AEGF closed FY2024–25 with total assets of ₹2.73 crore, up 60% from ₹1.70 crore a year earlier. Cash and cash equivalents rose from ₹1.37 crore to ₹2.21 crore, while reserves and surplus increased from ₹1.29 crore to ₹2.21 crore.

In the same year, its agri-entrepreneurs routed ₹623.67 crore of transactions—₹228 of rural commerce for every rupee of assets on AEGF’s books. Its total annual expenditure, salaries included, was ₹7.45 crore, giving it ₹84 of network throughput for every rupee spent.

Why would AEGF go for this multi-stakeholder partnership if they have such a good capital efficiency?

To answer this question, we would have to read AEGF’s Annual Reports from 2022-23 all the way up to 2024-25 for its vital signs to emerge.

The first strange thing you observe when you overlay the annual reports together is that reporting category of farmers changed from ‘Served’ to ‘Served/benefited’ to ‘Registered’.

The cadre grows by roughly four thousand a year. Commerce peaked in FY2023–24 and fell by a fifth the following year. Average throughput per agri-entrepreneur—the value of business passing through each entrepreneur, and therefore the transaction base from which commissions and service fees can be earned—has fallen by approximately 39% in two years.

It does not tell us what an entrepreneur actually earns, but it tells us that the pool of commerce available per entrepreneur is becoming thinner.

The farmer count moves the other way. The 2024–25 report counts 23.85 lakh farmers registered, against 14.40 lakh farmers served or benefited a year earlier.

A farmer can be registered in a digital diary without buying an input, selling produce, receiving credit or changing an agricultural practice. The network is registering farmers faster than it is trading with them.

And so could the purpose of PRAGATI be to create this full-stack agripreneurship model so that new revenue layers could be added to the same village interface, thereby increasing the throughput per agri-entrepreneur?

Corporate supply chains can use the entrepreneur for procurement and traceability. Banks can use her for customer origination and transaction facilitation. Foundations can use her to deliver development programmes. Climate organizations can use her to promote and measure regenerative practices. Governments can use her to connect farmers with schemes without constructing another last-mile cadre.

PRAGATI stacks all these functions onto one kiosk and hopes that their combined economics will create a viable livelihood. To understand, how these functions could be stacked, it is important to understand the AEGS’s existing geography

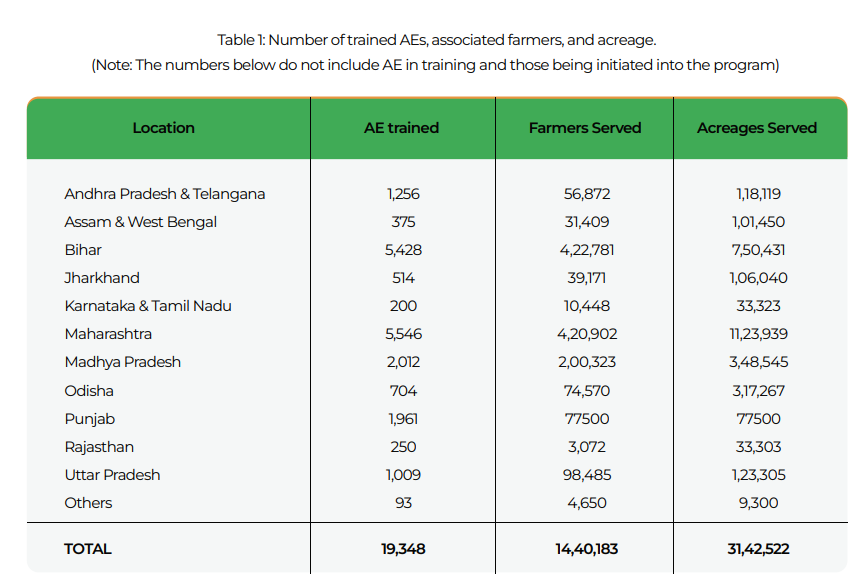

The FY2023–24 report records 5,428 entrepreneurs in Bihar, 5,546 in Maharashtra, 2,012 in Madhya Pradesh, 1,009 in Uttar Pradesh, 514 in Jharkhand, 375 across Assam and West Bengal, and 250 in Rajasthan.

That gives us 15,134 entrepreneurs across PRAGATI’s eight states, serving 12.16 lakh farmers over 25.87 lakh acres. These states accounted for 78% of AEGF’s entrepreneurs, 84% of its farmers and 82% of its acreage.

PRAGATI is not an expansion into new territory. It is a doubling of the network where the network is already thickest. Everything its four targets require has already been attempted in some form by the same organization, in the same geographies, at meaningful scale.

Let’s take Farmer incomes.

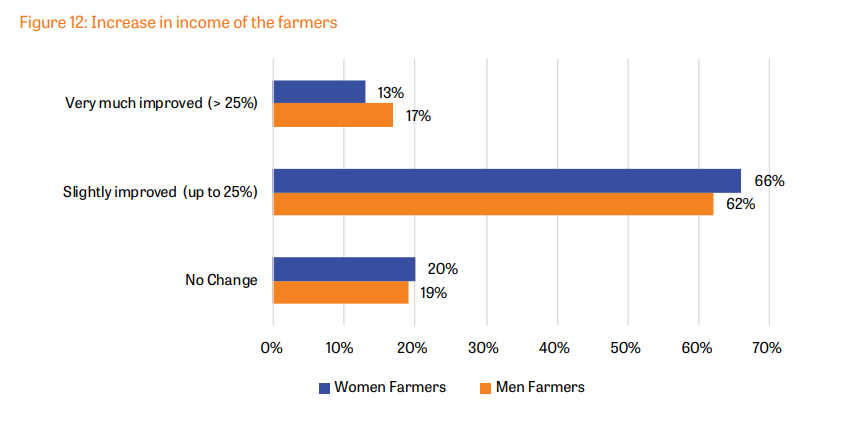

PRAGATI promises a 30% increase in the incomes of twenty lakh smallholders. AEGF’s most substantive farmer-outcome evidence comes from an impact study undertaken by 60 Decibels and reproduced in its 2022–23 and 2023–24 reports.

Roughly one farmer in six reports an income improvement above 25%. PRAGATI is promising an improvement of at least 30% across twenty lakh farmers. It’s evident that PRAGATI needs a robust outcome evidence study. There are data integrity issues at play.

The text above the farmer income chart says the following:

”79% of the farmers confirmed that their income has increased due to AE program and services provided by the AEs. Approximately half (48%) of the farmers accepted that the income has increased by half or more.”

The text above the farmer-income chart says that 48% of farmers reported income increases of 50% or more. The accompanying chart contains no category above 25%.

The 48% figure appears elsewhere in the same report. It refers to women agri-entrepreneurs whose income increased by 50% or more. An entrepreneur-income statistic appears to have travelled into the discussion of farmer incomes. The 2023–24 report repeats the claim and refers readers to a Figure 14 that does not exist in a document containing only eight numbered figures.

The 60 Decibels account describes a phone survey of 150 agri-entrepreneurs who had joined by the end of 2020, conducted across Maharashtra, Bihar and Assam. It does not explain the sample behind the farmer-income chart reproduced in AEGF’s reports. By March 2025, the network contained 22,560 trained entrepreneurs and 23.85 lakh registered farmers.

Mind you, Farmer income and entrepreneur income are not separate targets in this system. The entrepreneur is expected to deliver the advisory, input access, market linkage, finance and regenerative transition through which farmer incomes rise.

The reports also need to publish a state-wise distribution of entrepreneur incomes or the relationship between transaction value and net earnings.

There is also the challenge of density.

AEGF says its model is designed around each entrepreneur serving 150–200 farmers across one or two villages. The reported data shows a system operating considerably below that density.

Bihar’s AE count increased from 2,946 in FY2022–23 to 5,428 the following year—an 84% expansion. Over the same period, farmers served per entrepreneur fell from 113 to 78.

Rajasthan offers an even sharper warning. Its entrepreneur count remained at 250 across both reports, while farmers served fell from 8,320 to 3,072. That leaves approximately twelve farmers per entrepreneur.

Adding entrepreneurs does not automatically create more rural commerce. In saturated geographies, it can divide the existing transaction pool among more people. PRAGATI’s success will depend on whether its additional functions create paid work or merely add unpaid responsibilities to the kiosk.

Adding entrepreneurs does not automatically create more rural commerce. In saturated geographies, it can divide the existing transaction pool among more people. PRAGATI’s success will depend on whether its additional functions create paid work or merely add unpaid responsibilities to the kiosk.

Then comes yield

AEGF’s strongest published yield result comes from the Axis Bank Foundation programme in Maharashtra: a 12–15% increase in Bengal gram and up to 25% in onion, attributed to interventions including mulching and drip irrigation.

The FY2024–25 report records 192 field demonstrations reaching 40,992 farmers and attributes a 7–10% yield improvement to fertilizer optimization through soil testing.

These are useful results. But they are not the crops PRAGATI names.

PRAGATI promises a 15–20% yield improvement in paddy, maize and potato. Across the three reports, AEGF does not publish a comparable baseline, sample, control group or measured result for these crops.

AEGF’s clearest regenerative project is the Mitti Labs programme in Odisha, which seeks to move rice farmers from continuous flooding towards alternate wetting and drying.

The FY2023–24 report states an objective of reaching 12,000 farmers across 7,000 hectares. It reports delivery to 477 farmers over 2,389 acres through sixteen entrepreneurs.

That is 4% of the farmer target and approximately 14% of the area target. It may have been an early implementation year, but it remains the clearest regenerative delivery rate AEGF has published.

AEGF’s explicitly regenerative programs sit in Punjab, Odisha and Tamil Nadu. None is among PRAGATI’s eight states. PRAGATI has selected the states where AEGF’s entrepreneur and distribution networks are thickest, rather than those where its regenerative evidence is strongest.

It is important to delve deeper into the transaction mix layer.

The FY2024–25 report says 53% of farmers in its Maharashtra programme buy agricultural inputs directly from AEs. An entrepreneur who persuades a farmer to buy less fertilizer may improve the farmer’s economics while reducing her own commission.

The contradiction can be resolved only if someone pays the entrepreneur for the transition service—for advisory, soil testing, water savings, measurement, verification or assured procurement. Otherwise the system asks the entrepreneur to finance regeneration from her own foregone revenue.

If the entrepreneur earns from selling the farmer’s produce, rather than predominantly from selling inputs to her, higher farmer profitability and higher entrepreneur income begin to reinforce each other.

Credit and insurance transactions fell from ₹1.46 crore in FY2022–23 to ₹30 lakh in FY2023–24. The FY2024–25 report identifies insurance transactions of approximately ₹75 lakh, but its changed taxonomy prevents a direct comparison with the earlier combined category.

The reports place several activities under this label: working-capital loans to entrepreneurs, public subsidies unlocked for farmers, business-correspondent transactions and farmer credit linkages.

All are valid services. But a cash-in/cash-out transaction, a loan to an entrepreneur and production credit for a farmer are different outcomes. PRAGATI’s 50% target cannot be evaluated until financial inclusion is defined.

PRAGATI shows immense potential.

However, when I examine AEGF’s publicly available data, the following challenges are visible. Registration is outrunning engagement. Recruitment is outrunning transaction growth. Regenerative ambition conflicts with input-linked commissions. Financial inclusion remains undefined.

Can PRAGATI plumb deeper into its innards and make India’s largest privately-held entrepreneurship program work? Let’s see:) For starters, Can AEGF do a better Impact Study? Let’s hope.